Yup. Bought at the end of 2019, refinanced in late 2020. Currently have a 15 year mortgage at a fixed 2.1% APR. I literally cannot afford to give this up.

It’s less that I want to leave this house, specifically, and more that I just want out of this state. For multiple reasons unrelated to my good mortgage deal, I’m stuck here for the foreseeable future.

On the bright side, I never thought I’d actually own a house so I’ll take the win.

Ditto. 2.6%. Car loan at 3.2%. Can’t afford a new car, can’t afford to move these days. Yeah, it’s hard to bitch when you’re glad to have a home, but it’s a figurative “house arrest” when market forces trap you.

Don’t you have to renew it every 5 years?

I haven’t heard of having to renew mortgage interest rates. A fixed interest rate should be good for the life of the loan.

I’m at 2.875% on a 25-year loan. I never plan on moving.

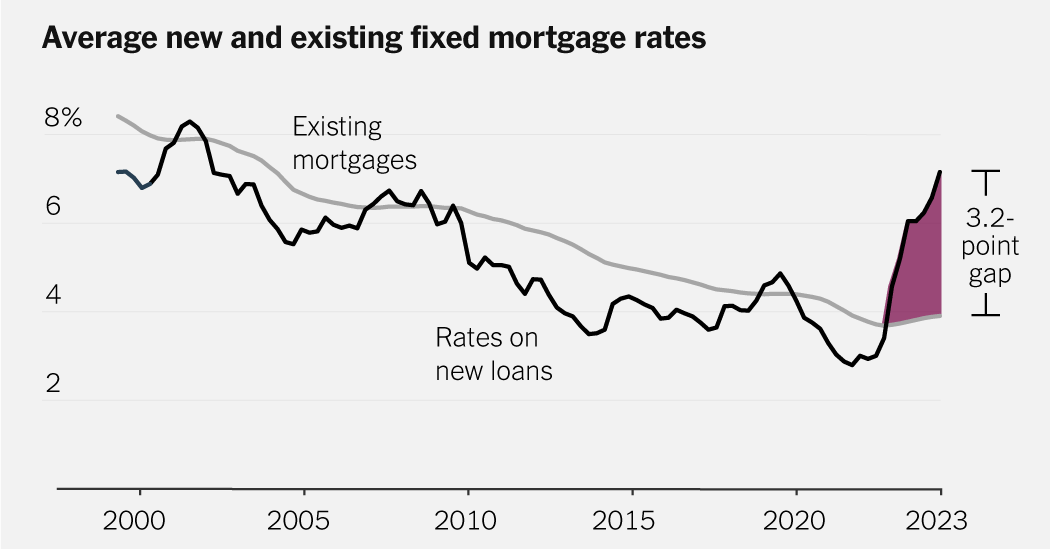

15 and 30 year fixed mortgages is pretty unique to the US.

I recently gave up my 3% mortgage from 2013 in exchange for a 7% mortgage. It hurts, but it was worth it to get out of Florida.

In the end, my housing costs actually didn’t change that much because my home insurance rates were skyrocketing.

but it was worth it to get out of Florida.

You could put almost any horrific thing in front of that phrase and it sound valid.

I had to keep my arm in a tub of fire ants for 5 minutes, but it was worth it to get out of Florida.

3.6 here (bought 22) and not fucking moving until rates are at least below 4 again. If that means I don’t ever move again then so be it

7-8% rates are bad by recent standards but not awful by historical standards. Depending on where I move and how much house I can get, I’d be willing to give up my 2.9% rate for something in that range.

There are a few other factors to consider right now, anyway. I’m a Houston resident, and this is supposed to be a particularly bad hurricane season along with a historic heat wave. My wife is terrified of the state’s newest right wing legislative push, as well. Michigan, Minnesota, and Washington is looking better and better as Texas brains are poisoned by MAGA media. And, despite having a gangbusters growth, my O&G employer decided to cut our bonuses from last year - so I’ve got one eye on the job market again. Our water bill jumped by 9% in a single year. Our interior roadways are falling apart, with no sign that the city or state plans to clean them up or improve access to public transit. HISD is being cannibalized by the governor’s cronies, so I won’t have anywhere to send my kids in a few years.

Would I pay an extra $500/mo to live in a state that isn’t run by pedophiles, bigots, and zealots? Absolutely. Bonus points if it got me out of the concrete jungle and put me in spitting distance of some decent mass transit.

People forget … If you refinance you are essentially selling the house to yourself with the lower rate, but Mr. Taxman will up your taxes to the current market value of your home, which is ridiculously high right now. Any savings in interest goes back into higher taxes. And now you will need more expensive insurance to cover the increase in home value.

This is not how things work in the US. At least not in the states that I’ve lived in: TX, CA, IL.

My current state, TX, regularly updates the property value assessment, so even if I don’t refinance, my property taxes goes up. With homestead exemption, the rise is capped at 10%, but over 2-3 years, it easily catches up to the market value.

But if you’re in CA or NV, that value assessment increase is capped at something like 2% or 1% annually, respectively. (Proposition 13) Creating situations where homes purchased 20 years ago are still paying really low property taxes compared to today’s buyers.

Isn’t that the way it should be? In Florida it’s capped low per year also…you bet the county raises it the max each year. My 95 year old neighbor has a yearly tax bill of 590, mine was 6k. If I stay in my house 50 years, my tax bill will be 1 tenth that of the new owners too.

Its good and bad. I’m conflicted about it, because I think everyone should pay a fair share of the property tax. The person that moved in 20 years ago and the person that moved in yesterday should shoulder the same amount of burden if their properties are equivalent.

But I also think its stupid that my property tax goes up just because some idiot decided to overpay for the house a few houses down the street.

I simply don’t like the idea that the property tax is tied directly to the appraised value of my house. It should really be tied to the size of the land that I am occupying and the total cost of running the city/county that I am in. If I build a fancy shed (insert any structure here) in my backyard, that shouldn’t really cause my taxes to go up even if it increases the value of my property. The only exception is if I change the dwelling type. If it goes from a single family home to a multifamily unit, then definitely the tax rate should be reevaluated, if it is using the infrastructure more.

2.875 here, my monthly payment is $545. I want to move, but it would be financially stupid to do so

Basically, unless the sale gets you enough to buy the next house in cash, it’s a bad idea, lol.

And people moved away from cities during COVID to decrease their cost of living and get a bigger place while still being able to work from home. They bought with lover interest rates in their mortgage.

Now employers want a return to office. The employees can’t afford to move back.

Also a lot of people have discovered that no one wants to live in rural areas because they fucking suck. That’s why there’s no people there.

Same story as everyone else. Bought pre-covid, refinanced, now sitting pretty. We desperately want to move, but I would have to make like $50k more a year for the same quality of life.

Rent it out or sell it and move. How is it not a wash for whatever u want to buy?

I’m in year 17 of my 5 year starter home. I can’t afford to upgrade now. I’m gonna die in this house.

Hey, don’t be so glum. You could die at work for example.

I work from home lol

Nice, you’re both right.